The relationship between psychology and finance is deeper than most people realize. While traditional economic theory assumes that individuals make rational decisions based on logic and available information, real-world behavior shows that emotions, biases, and cognitive errors play a major role in financial decisions. Understanding the psychology of money is essential not only for investors but also for anyone who wants to manage their personal finances effectively. This article explores how psychological factors influence financial behavior, investment decisions, risk tolerance, and long-term wealth building.

The Emotional Side of Money

Money is not just a mathematical tool; it is strongly connected to emotions such as fear, greed, anxiety, and confidence. These emotions often drive financial decisions more than logic does. For example, during a market crash, many investors panic and sell their assets at a loss because they are afraid of losing more money. On the other hand, during a market boom, investors may become overconfident and invest too aggressively, ignoring potential risks.

This emotional behavior leads to poor decision-making. Successful investors are not necessarily those who know the most about finance, but those who can control their emotions and stick to a long-term strategy.

Cognitive Biases in Investing

Cognitive biases are systematic errors in thinking that affect decision-making. In finance, these biases can lead to bad investments and financial mistakes. Some of the most common biases include:

Confirmation bias: Investors tend to look for information that supports their existing beliefs and ignore information that contradicts them. For example, if someone believes a stock will increase, they will focus only on positive news about that company.

Loss aversion: People feel the pain of losing money more strongly than the pleasure of gaining money. Because of this, investors often hold losing investments for too long, hoping they will recover, instead of selling and reinvesting in better opportunities.

Overconfidence bias: Many investors believe they know more than they actually do. This leads to excessive trading, higher risk-taking, and often lower returns.

Herd mentality: People tend to follow what others are doing. When everyone is buying a certain asset, more people buy it just because others are doing it, which can create market bubbles.

Understanding these biases is the first step to avoiding them and making better financial decisions.

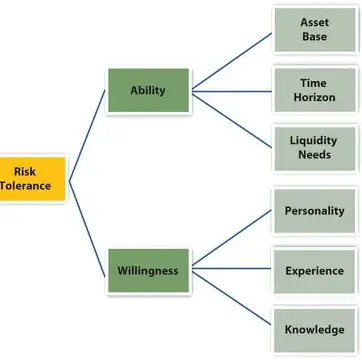

Risk Tolerance and Personality

Every investor has a different level of risk tolerance, which is influenced by personality, past experiences, income stability, and financial education. Some people are comfortable with high-risk investments such as stocks or cryptocurrencies, while others prefer safer investments like bonds or savings accounts.

Risk tolerance is also affected by age. Younger investors usually take more risks because they have more time to recover from losses, while older investors tend to be more conservative because they are closer to retirement.

Knowing your own risk tolerance is very important because investing in assets that are too risky can lead to emotional stress and bad decisions, especially during market volatility.

The Importance of Long-Term Thinking

One of the biggest psychological mistakes in finance is focusing too much on short-term results. Markets go up and down constantly, and short-term movements are often unpredictable. Investors who check their portfolios every day are more likely to make emotional decisions, such as selling during a temporary drop.

Long-term investors, however, focus on years or decades rather than days or weeks. Historically, long-term investing has been more successful because markets tend to grow over time despite short-term volatility.

Patience, discipline, and consistency are psychological traits that are often more important than financial knowledge when it comes to building wealth.

Financial Habits and Behavior

Financial success is not usually the result of one big decision, but of many small decisions repeated over time. Saving regularly, spending responsibly, avoiding unnecessary debt, and investing consistently are habits that lead to long-term financial stability.

Behavioral finance studies show that people who automate their savings and investments are more successful financially because they remove emotional decision-making from the process. Automation helps people stay consistent and avoid impulsive spending or investing.

Conclusion

The psychology of money plays a fundamental role in financial and investment decisions. Emotions, cognitive biases, risk tolerance, and financial habits all influence how people manage money and invest. Understanding these psychological factors can help individuals make better financial decisions, avoid common mistakes, and build long-term wealth.

In the end, successful investing is not only about numbers, markets, or strategies, but also about behavior, discipline, and emotional control. Those who understand their own financial psychology have a significant advantage in achieving financial stability and long-term financial success.